Tax Benefit on Home Loan

rimzim • July 29, 2022

The government has provided numerous benefits to home buyers to make the dream of home ownership available to as many citizens as possible. One of the most significant advantages of owning a home is the tax benefits on the home loan that come with it.

You can benefit from tax breaks by making several wise investments over the years. Among them, tax breaks on home loans are a long-term investment that will provide you with tax breaks for a longer period. A home loan qualifies for a tax deduction under Section 80C. If you want to buy your dream home, home loans offer numerous benefits in terms of housing loan tax benefits.

Continue reading to learn more about income tax benefits on home loans and how to take advantage of them.

Everything You Need to Know About Home Loan Tax Breaks

To begin understanding the income tax benefit on home loans, we must first understand the home loan process.

What Exactly is a Home Loan?

A home loan is a large amount of financial assistance that lenders provide to help you purchase your dream home. Depending on loan eligibility and funding norms, lenders can pay between 75 and 90 percent of the cost of the home you purchased.

You can use the home loan eligibility calculator to determine your eligibility for a home loan. Following your initial down payment, lenders will disburse the loan amount in installments or in full, depending on the stage of construction of the property. In the event of partial loan disbursement, the financial institution will only charge interest on the amount disbursed. In the case of a fully disbursed loan, EMI will begin. The repayment of principal and interest is included in the EMI.

Tax Breaks on Home Loans

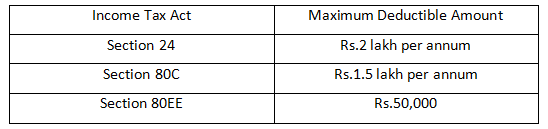

The table below summarizes the tax benefits available under the corresponding sections of the Income Tax Act of 1961.

The Union Minister of India announced in 2020-21 that all previous regimes of income tax rebates on home loans would be extended until 2024. The following are the advantages of a home loan:

Interest Deduction on Principal Repayment

The principal amount and interest amount are two components of the EMI that you pay. You can deduct the amount you repaid on account of principal in the EMI for a self-occupied property under section 80 C of the Income Tax Act of 1961. If you have a second home where your parents live or it is empty, it is also considered self-occupied property.

You will be able to claim a tax deduction of up to 1.5 lakh on the principal amount paid in EMIs for both houses purchased with home loans. If you rent out the second house, it is considered a let-out property, and you are still eligible for the home loan tax credit. You can also claim the registration and stamp duty fees you paid when you bought your home.

Deduction on the Payment of Interest

The interest paid on a home loan is also deductible as a tax deduction. You are eligible for a home loan tax benefit of up to 2 lakhs for a self-occupied home under section 24 of the Income Tax Act. If you have a second home, the total tax deduction on a home loan for two homes in a fiscal year should not exceed 2 lakhs.

If it is a rented property, there is no maximum limit for claiming interest. The loss you can claim under Income from House Property, however, is limited to Rs. 2 lakhs. The remaining loss can be carried forward for an additional eight years for use in adjusting the Income from House Property.

Additional Deduction Under Section 80EE

If you took out a home loan during the fiscal year 2016-17, you are eligible for this tax break. If you meet the following conditions, you are eligible for an additional deduction of Rs. 50,000 in addition to the deduction of Rs. 2 lakhs on interest paid under section 80EE.

- The loan amount should not exceed Rs. 35 lakhs, and the property against which the loan is taken should be worth Rs. 50 lakhs.

- You should have received the sanction between April 1st, 2016, and March 31st, 2017.

- This deduction only applies to residential property and first-time home buyers.

Extra Deduction Under Section 80EEA for a Low-Cost House

You can claim an additional deduction of up to Rs. 1.5 lakh on home loan interest paid. To qualify for the home loan tax credit under Section 80EEA, you must meet the following requirements:

- The maximum stamp value for residential property should be 45 lakhs.

- You must have applied for the loan between April 1, 2019, and March 31, 2020.

- On the date the loan is approved, you must be a first-time home buyer.

- You must not be eligible to claim deduction under section 80EE to claim deduction under this section.

Deductions for Joint Home Loans

Borrowers must be joint owners of the property and can claim deductions of up to 2 lakhs on interest and 1.5 lakhs on the principal on the home loan.

Tax Deduction For Joint Home Loan

If you take out a home loan jointly, each borrower can claim a deduction for home loan interest up to Rs. 2 lakh under Section 24(b) and a tax deduction for principal repayment up to Rs. 1.5 lakh under Section 80C. When compared to a single applicant home loan, this doubles the number of deductions available. It is required, however, that both applicants be co-owners of the property and service the EMIs.

Home Loan Tax Advantages of Having a Second Property

Tax benefits are currently available on payable interest under current legislation. You may claim the entire amount of interest paid.

To help borrowers save more on taxes, it has been proposed that the second self-occupied home can also be claimed as a self-occupied one.

How Do I Claim Tax Breaks for Home Loans?

It is simple to claim tax benefits on a home loan. The steps for claiming your tax deduction are outlined below.

- Determine the tax deduction that will be claimed.

- Confirm that the property is in your name or that you are a co-borrower on the loan.

- Provide your employer with your home loan interest certificate to adjust the tax deductible at the source.

- If you do not complete the preceding step, you must file your tax return on your own.

- If you work for yourself, you are not required to submit these documents anywhere. Simply keep them on hand in case the IT department has any questions in the future.

How to Calculate Home Loan Tax Benefits

Using an online calculator to calculate your tax benefits on a home loan is the simplest way. Simply enter your home loan information and click calculate to see a detailed tabulation. The following information is typically required:

- Loan Amount

- Loan Tenure

- Interest Rate

- Commencement Date

- Gross Annual Income

- Existing Deduction Under 80C/D

Share this article on WhatsApp

Also read: