Documents Required for Loan Against Property

rimzim • January 17, 2022

A loan against property is a secured loan obtained against a residential property held as collateral with the lender, and it aids in the provision of funds when needed. The interest rates on a secured loan are competitive, and you can repay the loan in manageable instalments. Home First Finance Company provides a simple process and end-to-end management with a dedicated loan against property specialist to ensure timely disbursements.

This article will help you understand the concept of a loan against property secured by real estate. It will also provide you with a good understanding of the application process and the documents required for a loan against property. In addition, we have listed a few important things that you should keep in mind when applying for this type of loan.

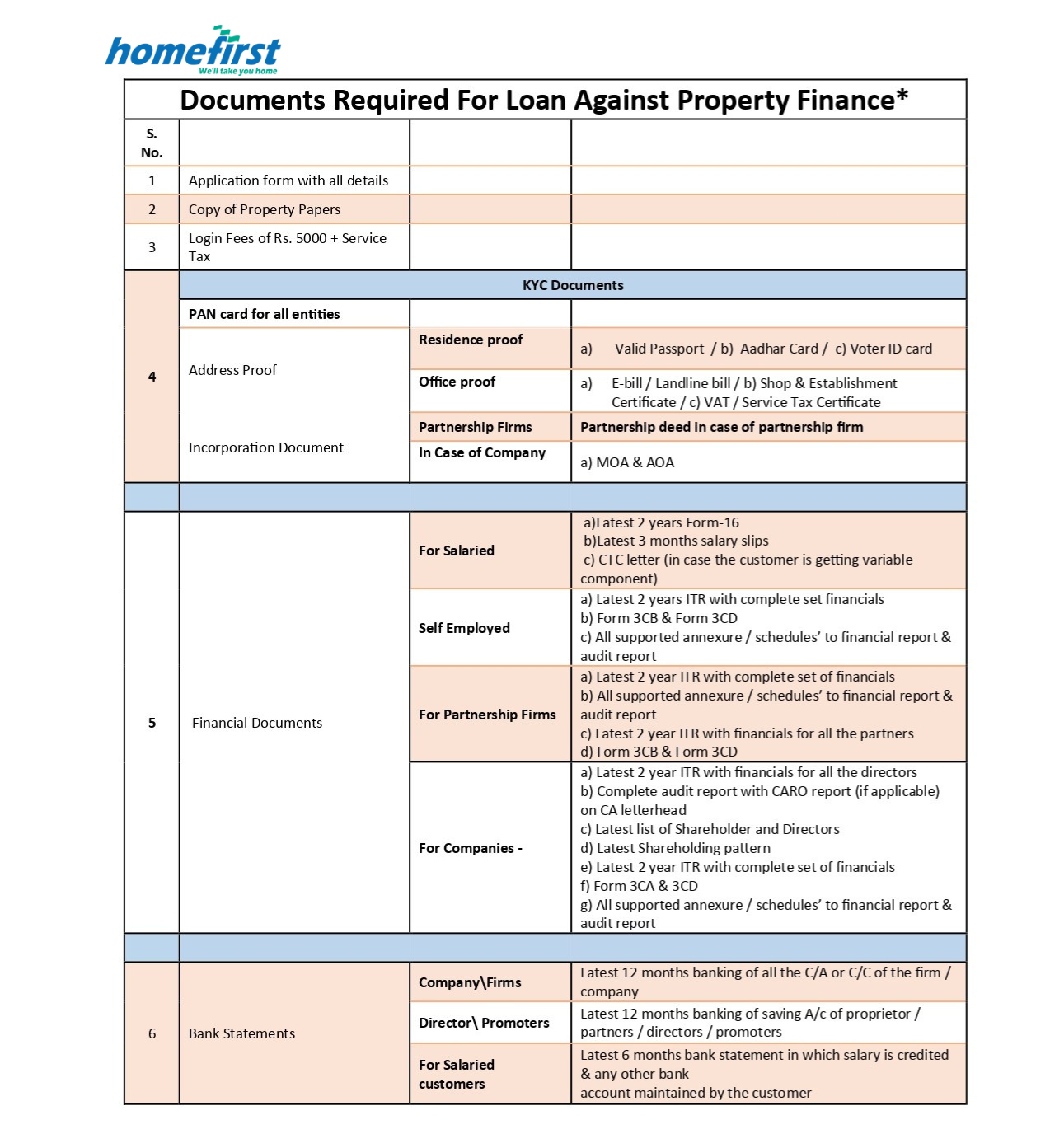

Documents Required for Loan Against Property:

For Salary Candidates:

- Identification proof (any of the following):

- PAN number

- Passport, Driver’s License, and Voter ID

- Employee ID Passbook at the Bank

- Ration book

Address Verification (Any of the following):

- Utility bill (telephone, electricity, water, gas) – less than 2 months old

- A letter from a recognized public authority confirming the customer’s address

- Bank account statement or bank passbook

- Ration card

- Ration card Voter ID

- LIC policy/receipt

Proof of Residence Ownership (Any of the following):

- Property documentation

- Electricity bill

- Maintenance bill

Income Documentation (Any of the following):

- Payslip (Last 2 months) (Last 2 months)

- IT returns

- Increment or promotion (for 3 years)

- Form 16

- Employer’s Certified Letter

Proof of Employment (Any one of the following):

- Letter of current job appointment (if more than 2 years have been spent in the same job)

- Certificate of current employment

- Certificate of experience (including previous job certificate or appointment and relieving letter)

- Last six months’ bank statement Salary account bank statements

- Existing debt: In the case of an existing loan, the sanction letter and payment track record must be submitted.

- (If applicable) investment proof: fixed deposit, fixed assets, shares, etc.

- All property documents should be copied: Sales deed/agreement copy, share certificate (if society formed), and most recent maintenance bill

- Advance processing cheque: used to process loan documents in preparation for sanction.

For Self-Employed Individual/Businessman:

Proof of Identification

- Proof of Identification

- Address Proof

Proof of Residence Ownership (Any of the following):

- Property documentation

- Electricity bill

- Maintenance bill

- Office address

Proof of ownership (Any one of the following)

- Property documentation

- Electricity bill Service bill

Evidence of a Company’s Existence (Any one of the following)

- Agreement/sale deed (executed)

- Saral clone (3 years old)

- Tax registration copy Company registration licence

Income Documentation (Any of the following):

- Last three years Income tax returns and income computations of the applicant, duly attested by a Chartered Accountant

- Balance sheet and profit and loss accounts audited, including tax audit report, if applicable

- Statement from the bank: Bank statement from the previous year (both savings and current)

- All property documents should be copied: Sale deed/agreement copy, share certificate (if a society is formed), and maintenance bill

- Advance processing cheque: used to process loan documents in preparation for sanction.

- Photograph in passport size and colour

- (If applicable) investment proof: fixed deposit, fixed assets, shares, etc.

- Existing debt: In the case of an existing loan, the sanction letter and payment track record must be submitted.

- Certificate of Professional Degree: (in case of professionals).

Eligibility for Loan Against Property?

Before we get into the various documents needed for loan approval, let’s go over the eligibility criteria for a loan against property:

- The applicant must be the legal owner of the property being offered as security.

- The applicant’s age must be at least 21 years old.

- The applicant should be salaried or self-employed and have a steady and consistent

- An applicant must be salaried/professional or self-employed.

How to Apply for a Loan Against Property?

It is very simple to apply for a loan against property with Home First Finance Company. All you need to do is ensure that all of your loan application documents are complete and accurate.

- To apply for a loan against property, follow these steps:

- Fill out the loan application form completely and include two recent passport-size photos of yourself.

- Please include all requested documents.

- Submit the attached form and documents to the nearest HomeFirst branch to begin your loan application process today.

Things to Keep in Mind when Applying for a Loan Against Property:

Here are a few quick pointers to keep in mind when applying for a loan against property:

Property should be free of contention

Before applying for a loan, ensure that the collateral you provide is free of any disputes. Uncertain property papers and ownership disputes among property owners can lead to loan application rejection.

The loan amount must be manageable

The bank makes the loan based on the collateral provided. They do, however, expect all borrowers to pay their EMIs on time. Payment default can lead to problems with the bank in the future.

Choose the appropriate tenure

When deciding on a tenure, it is critical to consider your repayment capacity as well as the interest rate. You can use an EMI calculator to figure out how much you’ll owe the lender based on your interest rate and loan amount. This tool can assist you in selecting the appropriate tenure.

Check the value of your home

Make this a priority before applying for a loan. Only if the property was purchased more than three years ago will a bank consider the realizable value rather than the market value. In the case of a purchase within the next three years, the lower of the registered value or the realizable value is taken into account. Furthermore, you are eligible for a loan of 60% of the value accepted by the bank.

Conclusion:

Taking out a mortgage loan is a big decision that requires careful consideration. HomeFirst understands how hard you work to make your dreams a reality and provides you with affordable loans. We also have simple eligibility requirements, minimal documentation, and quick loan disbursement upon approval.

You can use our Loan Against Property EMI Calculator to figure out how much you’ll have to pay each month. This way, you can choose the appropriate loan term and amount and plan your finances before applying for the loan. We believe in streamlining the loan application process so that you can get the money you need quickly.

Share this article on WhatsApp

Also read: