Benefits of Home Loan for the First Time Home Buyers

rimzim • June 26, 2021

Don’t own a home yet? What are you waiting for? Money? Okay, that makes sense. But hold on, you may not need as much as you think you do. There are loads of benefits that are offered to first-time homebuyers so maybe it’s time to prepone your home buying plan. Let’s hit it!

- Deduction on Home Loans Interest Paid – You can claim an additional tax deduction of Rs.50,000 under Section 80 EE of the Income Tax Act, 1961. This deduction is over and above the current limit of Rs.2,00,000 which is availed under Section 24. But hold your jumping for now. Here are the conditions under which this benefit can be availed:

- The additional deduction is applicable only on the interest portion of the loan which is taken for a self-occupied property.

- The benefit is applicable only for first-time home buyers. And we’re all working here under this assumption.

- The value of the house is not more than Rs.50,00,000 and the loan taken is not more than Rs.35,00,000. Benefits are meant for people who need it, right!

- The Home Loan should’ve been sanctioned between April 2016 and 31st March 2017.

Do you fulfill these criteria? Okay, you can jump now!

- Tax Benefits in absence of HRA – Even if you’re not getting any HRA from your employer, fret not. Here comes Section 80GG under which you can avail of some tax benefits as well. This provides for deduction of any expenditure incurred by an individual, in excess of 10% of their total income for rent payment, for a furnished/unfurnished accommodation if they are not granted HRA by their employer or are self-employed. But hold on, conditions ahead. The excess expenditure must not exceed Rs.2,000 per month or 25% of their total income for the year, whichever is less.

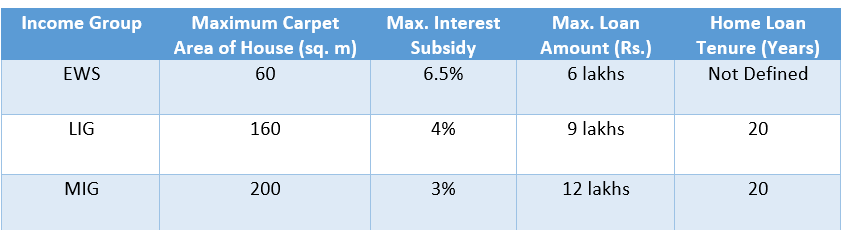

- Pradhan Mantri Awas Yojana – I know you were waiting for this. Here it is. The PMAY scheme is for home buyers from the Economically Weaker Sections (EWS), Lower Income Group (LIG), and Middle-Income Group (MIG). If you are from one of these sections, GoI is here for you. You can claim tax subsidy (not benefits) on Home Loans. Here are the parameters to decide how much subsidy you can get:

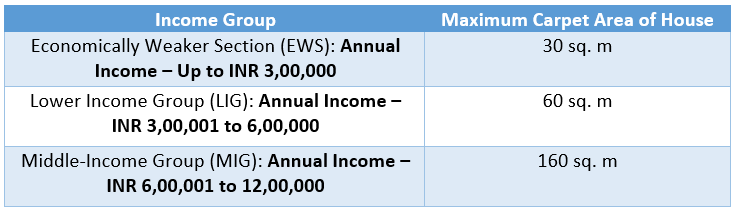

And how do you define income groups?

Share this article on WhatsApp

Also read:

Home Loan Affordability Using Income

Home Décor Furniture: Transform Your Space With Home Décor Ideas

Home Décor : Decorate Your Space with Home Décor Ideas

Factors to Consider Before Buying the Right Property in India

All You Should Know About Home Loan Disbursment Process

Your Responsibilities as a Borrower

Spread the knowledge